The Weekly Wealth Watch

May 25, 2026

The Markets

“The first step toward getting somewhere is to decide you’re not going to stay where you are.” — John Pierpont Morgan (J.P. Morgan)

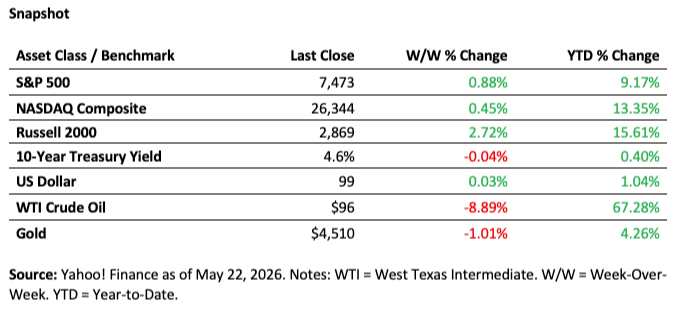

U.S. equity markets moved higher this week, with gains broadening beyond large-cap technology and participation improving across market segments. The S&P 500 advanced +0.88%, lifting its year-to-date gain to +9.17%. Technology shares also continued higher, with the NASDAQ Composite rising +0.45%, extending its year-to-date return to +13.35%. Small-cap stocks stood out as the week’s strongest performer, with the Russell 2000 gaining +2.72%, pushing its year-to-date advance to +15.61%. The leadership from smaller companies suggests improving breadth and a willingness among investors to move beyond the market’s largest names.

In fixed income, the 10-Year Treasury yield declined –0.04%, finishing the week at 4.6%. The modest pullback in yields alongside stronger equity performance provided a supportive backdrop for risk assets and eased some pressure on rate-sensitive segments of the market.

Currency markets were relatively stable, with the U.S. dollar rising +0.03%, bringing its year-to-date gain to +1.04%. The muted move in the dollar had little impact on broader market trends during the week.

Commodities softened. WTI crude oil declined –8.89%, though it remains substantially higher for the year at +67.28%, reflecting both prior strength and continued sensitivity to supply expectations and geopolitical developments. Gold also moved lower, declining –1.01%, trimming its year-to-date gain to +4.26% as easing rate pressures and steadier risk sentiment reduced demand for defensive positioning.

Taken together, the cross-asset backdrop reflects a market that remains constructive and increasingly broad-based. Equities moved higher, small caps regained leadership, yields edged lower, and commodity markets cooled after a strong run. Consistent with J.P. Morgan’s observation, investors appear increasingly willing to reposition toward opportunity as confidence in the broader market environment continues to improve.

Software vs. Semis: Skate to Where the Puck Is Going

“I skate to where the puck is going to be, not where it has been.” — Wayne Gretzky

Everybody Loves Semiconductors

And honestly? We get it.

Semiconductor stocks have been hotter than a sidewalk in Arizona.

According to World Semiconductor Trade Statistics, global semiconductor sales exploded 88% year-over-year in March — the fastest growth ever recorded.

Meanwhile, NVIDIA continues behaving less like a company and more like a financial Marvel superhero:

- Revenue growth: +85%

- EPS growth: +131%

- Market cap: Over $5 trillion

At this point, NVIDIA earnings calls may need their own halftime show.

But Here’s the Catch…

“Trees don’t grow to the sky.” — European proverb

When everyone crowds into the same trade, markets can get a little … cramped.

That doesn’t mean semiconductors are doomed. It just means investors may eventually look for the next opportunity.

And that’s where software enters the chat.

While semiconductor stocks sprinted higher, many software companies quietly sat in the corner like the kid nobody picked for dodgeball — stable, profitable, and mostly ignored.

That may create opportunity.

AI May Actually BOOST Software Demand

“The real problem is not whether machines think but whether men do.” — B. F. Skinner

Many investors worry AI will destroy software companies.

But history suggests technology often creates more demand, not less.

Economist William Stanley Jevons noticed this way back in the 1800s:

- When coal became more efficient, people used more coal, not less.

That idea became known as the “Jevons Paradox.”

Today’s version?

- If AI makes software cheaper and easier to build …

- Companies may end up using more software everywhere.

More apps.

More automation.

More cloud services.

More cybersecurity.

More data management.

In other words: Fewer boring coding tasks, more high-value problem solving.

Old Economy Stocks Are Sneakily Benefiting, Too

“The future is already here — it’s just not evenly distributed.” — William Gibson

One of the biggest surprises of the AI boom is that it’s helping “old economy” sectors, too.

Industrials, materials, and utilities are benefiting from:

- Data center construction

- Power grid upgrades

- Supply chain optimization

Apparently, even boring utility companies can become exciting if you tell investors they’re powering AI servers.

Markets are funny like that.

Winners and Losers

“Success is where preparation and opportunity meet.” — Bobby Unser

The market story today isn’t just “technology wins.”

It’s:

- Which technology?

- At what price?

- And what benefits next?

Semiconductors have clearly led this cycle.

But leadership rotates.

Sometimes the best opportunities come from areas investors temporarily forgot about while chasing whatever stock is trending on financial television that week.

Our view remains balanced:

- Stay optimistic on technology long term.

- Protect gains where momentum became crowded.

- Stay open-minded about the “next wave” of beneficiaries.

Because markets rarely reward investors for staring in the rearview mirror.

Human Interest: The Inner Voices of Investing

“The test of a first-rate intelligence is the ability to hold two opposed ideas in mind at the same time.” — F. Scott Fitzgerald

Every investor has multiple “voices” in their head.

One says:

“Buy more tech!”

Another says:

“Maybe take some profits…”

And another quietly whispers:

“Did we really just pay how much for that stock?”

That’s normal.

Good investing often means balancing optimism, caution, and curiosity at the same time.

Also, coffee. Lots and lots of coffee.

Fun Facts & Figures

- 💻 The first computer “bug” was an actual moth found inside a machine in 1947.

- 🧠 AI models today can process information faster than humans, but still can’t reliably explain why printers stop working.

- ⚡ Data centers may soon consume more electricity than some small countries.

- 📈 The S&P 500 Information Technology Index remains one of the market’s biggest earnings engines.

- 🏒 Wayne Gretzky once scored 215 points in a single NHL season. Markets call that “outperformance.”

On This Day in History – May 25

“The more you know about the past, the better prepared you are for the future.” — Theodore Roosevelt

- 🚀 1961: John F. Kennedy announced America’s goal of landing a man on the Moon.

- 🎬 1977: Star Wars premiered in theaters and changed pop culture forever.

- 🧪 1953: Scientists publicly announced the discovery of DNA’s double-helix structure.

- 🏁 1935: Track legend Jesse Owens set three world records in less than an hour.

Sources & Footnotes:

- World Semiconductor Trade Statistics — Global semiconductor sales data, May 2026.

- Bureau of Labor Statistics — Software employment projections and labor market data.

- U.S. Census Bureau — Information technology manufacturing orders.

- S&P Global and YCharts — Sector, factor, and industry performance data.

- WCG analysis and commentary, May 2026.

Disclosures:

- Securities offered through LPL Financial, Member FINRA/SIPC. Investment Advice offered through WCG Wealth Advisors, LLC, a Registered Investment Advisor. WCG Wealth Advisors, LLC is a separate entity from LPL Financial.

- Bond yields are subject to change. Certain call or special redemption features may exist which could impact yield. (118-LPL)

- The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States. Indexes are unmanaged and cannot be invested in directly. (102-LPL)

- The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index. Indexes are unmanaged and cannot be invested in directly. (112-LPL)

- The fast price swings in commodities will result in significant volatility in an investor’s holdings. Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors. (122-LPL)

- There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. (26-LPL)

The Russell 2000 Index is generally representative of the 2,000 smallest companies by market capitalization in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index. Indexes are unmanaged and cannot be invested in directly. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Bonds are subject to availability, change in price, call features and credit risk. The fast price swings in commodities will result in significant volatility in an investor’s holdings. Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors.

Securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC.