Market Strategy

by Talley Leger, Chief Market Strategist

June 12, 2026

Signal vs. Noise: Cool “Core” CPI, Hot “Headline” CPI

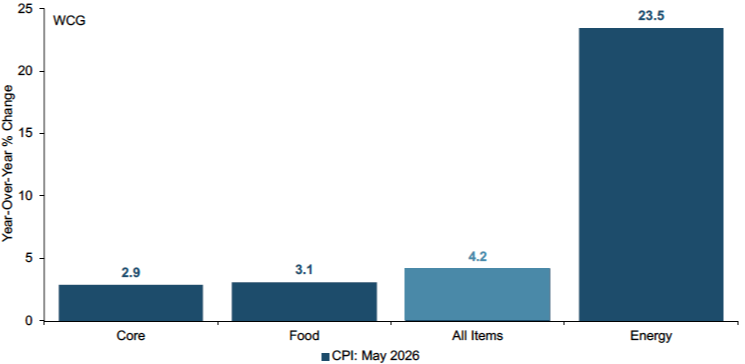

What Happened: As expected, the Bureau of Labor Statistics’ (BLS’) Consumer Price Index (CPI) for All Urban Consumers (read: “headline” CPI) popped 0.5% month-over-month (M/M) and 4.2% year-over-year (Y/Y) in May. By contrast, the CPI for All Items Less Food & Energy (read: “core” CPI) rose by a less-than-expected 0.2% M/M and 2.9% Y/Y in the same time frame (see the chart below).

War-Flation: Clearly, the Iran war-related impact on the CPI for Energy, which soared 23.5% Y/Y last month, is driving a wedge between “headline” heat and “core” coolness. While the geopolitical oil supply shock continues, the saving grace is that it was anticipated by markets and investors are coming to understand the mechanical, textbook divergence in inflation trends.

Underlying inflation of 2.9% Y/Y remains relatively subdued

Sources: BLS, WCG, 6/10/26. Notes: Core = All items minus food and energy. CPI = Consumer Price Index.

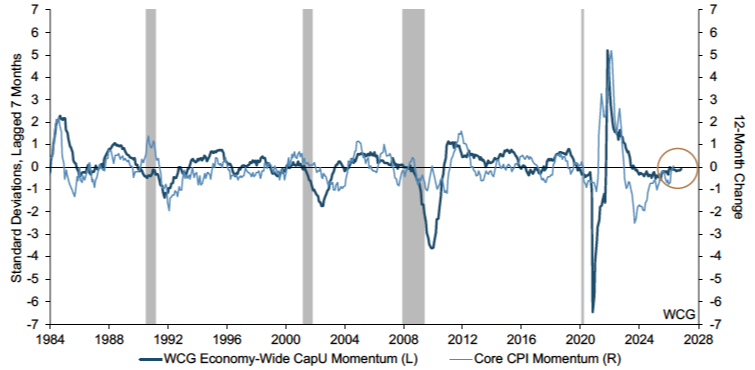

Keep Calm: Perhaps level-headed investors like us are right to “keep calm and continue” when it comes to “transitory” energy inflation pressures. Historically, persistent run-away inflation is spurred by demand-related stress on the productive capacity of the domestic economy (see the chart below).

Non-Inflationary Equilibrium: Judging by my “normalized” composite of industrial and labor capacity utilization (capu), however, the pace of “core” CPI inflation is almost exactly where it should be:

- Currently, economy-wide capu momentum is resting just below the “horizon” line. Specifically, a z-score of -0.1 standard deviation (SD) is virtually indistinguishable from the long-term average of 0.0, signaling that overall capacity utilization is close to perfectly balanced.

- Looking ahead, my indicator leads the “core” CPI inflation rate by seven months, meaning a statistically neutral reading today points to a benign, trend-like inflation impulse tomorrow. In other words, structural inflation trends seem well-anchored because capacity utilization isn’t flashing signs of overheating.

Core inflation momentum is almost exactly where it should be

Sources: BLS, FRED, WCG, 6/10/26. Notes: CapU = Capacity Utilization. Vertical gray bands = US economic recessions. Momentum = Year-over-year change.

Bottom Line:Policymakers and investors who are over-reacting to hot “headline” inflation are likely missing the forest for the trees. If broad industrial and labor capacity aren’t strained, the energy-fueled spike in “war-flation” may prove temporary. Indeed, my analysis isolates and quantifies current inflationary pressure as an “exogenous” supply-side shock, not an “endogenous” demand-driven shift.As such, we question the need for the Federal Reserve (Fed) to raise the federal funds rate at this juncture.

Portfolio Strategy

by Jim Worden, CFA®, CMT®, CAIA®, Chief Investment Officer

June 12, 2026

Space: The Final Frontier

With virtually everyone seeming to weigh in, and with many proclaiming they know everything about SpaceX and its upcoming IPO, I wanted to share a few thoughts.

Access to Shares, Dilution, and SPVs

Some investment vehicles may have direct exposure to SpaceX shares. Others may have access through a Special Purpose Vehicle (SPV). SPVs are structured differently and may be valued differently than direct shares of SpaceX. They may also include additional fee layers.

It is critical for investors to understand that any fund that currently has exposure to SpaceX can have that exposure diluted, sometimes significantly, with new inflows into the fund. This is because funds may not be able to easily access more shares of SpaceX. So if fund XYZ, which is not a real investment, has 20% exposure to SpaceX and hundreds of millions of dollars come into that fund, it may not continue to have 20% exposure to SpaceX. Depending on how much money has come in, the exposure could be significantly less.

Valuation

Some firms are looking at the limited financial information available on SpaceX and trying to back out what the value should be, possibly using some sort of discounted cash flow model. Others are looking at the potential for SpaceX and treating the “moonshot” scenario as the baseline. The reality for SpaceX is likely somewhere in between. For companies in high-growth mode and at the epicenter of the AI buildout, there is a clear tailwind of CAPEX that could lift shares and valuation higher for longer than what might seem rational. That said, large CAPEX can also weigh on margins, cash flow, and near-term profitability.

Remember the quote attributed to John Maynard Keynes: “Markets can remain irrational longer than you can remain solvent.”

Index Providers and Active Managers

In private conversations, I have heard from some fund managers who own SpaceX that other active managers want exposure and do not have any. Until we see the actual activity, however, this is conjecture. If SpaceX becomes one of the largest market-cap companies after its IPO, some benchmark-sensitive active managers may evaluate whether to add exposure to manage tracking error. Other active managers may believe SpaceX is a potentially attractive long-term investment and may seek to own more than a market-cap weight. These are potential outcomes, not guarantees.

The IPO is also interesting because there is a divergence between Nasdaq and S&P Dow Jones Indices. Nasdaq’s revised methodology says fast-entry candidates ranked in the top 40 and meeting applicable eligibility criteria may be added to the Nasdaq-100 after 15 trading days, subject to the 3x float cap where applicable. By contrast, S&P Dow Jones Indices said it will not change existing eligibility criteria for the S&P 500, S&P MidCap 400, or S&P SmallCap 600, including the 12-month IPO seasoning period, financial viability screens, and minimum investable weight factor requirements. This divergence may feed both the narrative of waiting and the narrative of getting in early. [1][2]

My Take on It

SpaceX’s Connectivity segment, driven by Starlink, is the company’s largest reported revenue driver, but SpaceX overall still reported a net loss in 2025. SpaceX will likely continue to launch more satellites, with the goal of improving latency, bandwidth, and broader mobile connectivity over time. [3]

The AI component remains investment-intensive, but the reported compute agreements with Google and Anthropic are meaningful. TechCrunch reported that Google agreed to pay SpaceX $920 million per month from October 2026 through June 2029. Axios separately reported that Anthropic agreed to pay SpaceX $1.25 billion per month through May 2029. The agreements reportedly include termination provisions, so investors should avoid treating those revenue streams as guaranteed. Those contracts could help support AI cash flow if SpaceX can deliver the committed capacity and if demand remains durable. [4][5]

The investment into spectrum, the EchoStar transaction, the developing Terafab project with Tesla and Intel, and other capital spending projects may squeeze the financials and make valuation more difficult to underwrite. The Terafab language should be viewed carefully, as reporting on the S-1 indicates the project remains in an early framework stage rather than a fully committed buildout. [6][7]

On the flip side, the EchoStar spectrum transaction and the broader Starlink Direct to Cell opportunity could help expand SpaceX’s mobile connectivity business. The T-Mobile/Starlink service is already positioned around satellite connectivity for areas beyond traditional cellular coverage, and EchoStar’s agreement with SpaceX would enable Boost Mobile subscribers to access next-generation Starlink Direct to Cell service, subject to approvals and closing conditions. [7][8]

Taken together, I think SpaceX looks potentially interesting as a long-term growth investment with a wide moat. The question for all investors is what price one should pay today for that potential growth and moat.

Sources

[1] Nasdaq, “Nasdaq-100 Index Methodology FAQ,” May 2026.

[2] S&P Dow Jones Indices, “S&P Dow Jones Indices Consultation on Treatment of MegaCap Companies Results,” June 4, 2026.

[3] Via Satellite, “SpaceX’s IPO Filing Gives First Look Into Company’s Financials,” May 20, 2026.

[4] TechCrunch, “Google Will Pay SpaceX $920M Per Month for Compute,” June 5, 2026.

[5] Axios, “Anthropic Is Paying SpaceX $15 Billion Per Year,” May 20, 2026.

[6] Reuters, “Intel to Join Musk’s Terafab Mega AI Chip Project,” April 7, 2026.

[7] EchoStar, Form 8-K / investor filing regarding SpaceX spectrum transaction, September 2025.

[8] T-Mobile, T-Satellite with Starlink service description.

Definitions

The BLS is a government agency that measures inflation, jobs, and spending in America.

The CPI tracks prices over time and shows how much everyday living costs are rising.

Industrial CapU measures factory output against full limits and shows how hard factories are running their machines.

The Unemployment Rate (UR) shows the number of jobless people looking for work as a percentage of the total labor force.

Economy-Wide CapU Momentum is a normalized sum of annual changes in the industrial capu rate and annual changes in the UR. It tracks how quickly or slowly overall factory and labor use is changing.

SD measures how spread out numbers are and tells us if data sit close to or far from average.

A z-score transformation changes raw data into standard scores and shows how many SDs a given point is from its average.

The Fed is the United States’ central bank, which influences interest rates, money supply and inflation to keep the economy and employment stable.

The federal funds rate is the target interest rate for overnight bank loans and sets the baseline cost for borrowing money.

Special Purpose Vehicle (SPV): A legal entity created for a specific investment purpose. In this context, an SPV may hold shares of a private company and provide indirect exposure to investors.

Share Dilution / Exposure Dilution: Traditional share dilution refers to a reduction in ownership percentage when a company issues additional shares. In this context, exposure dilution refers to a reduction in a fund investor’s percentage exposure to an underlying holding, which can occur when new assets enter a fund and the fund cannot acquire additional shares of that same holding.

Discounted Cash Flow (DCF): A valuation method that estimates the present value of a company based on projected future cash flows.

CAPEX: Capital expenditures, or money spent by a company to acquire, build, or improve long-term assets.

Tracking Error: A measure of how much a portfolio’s performance differs from its benchmark.

Market-Cap Weight: The weight a company would have in an index based on its market capitalization relative to the market capitalization of the other companies in the index.

Initial Public Offering (IPO): The process by which a private company offers shares to public investors for the first time.

Investable Weight Factor (IWF): An index methodology measure used to reflect the portion of a company’s shares that is generally available to public investors.

Free Float: Shares that are publicly available for trading, excluding shares that may be closely held or otherwise restricted.

Moat: A durable competitive advantage that may help a company protect profits and market share over time.

Disclosures

This material is for informational and educational purposes only and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security. Any opinions expressed are those of the author and are subject to change without notice.

Private companies, IPOs, SPVs, and funds with private-company exposure involve significant risks, including valuation uncertainty, limited liquidity, limited transparency, higher fees, potential conflicts of interest, and the possibility of substantial loss.

Index inclusion is not guaranteed and is subject to the rules, discretion, timing, and eligibility criteria of each index provider. Any discussion of possible index inclusion is based on currently available information and may change.

Forward-looking statements, including statements about potential growth, profitability, valuation, index demand, revenue growth, satellite deployment, AI demand, or future investor behavior, are inherently uncertain and should not be relied upon as guarantees of future results.

Any discussion of SpaceX, Starlink, Terafab, EchoStar, T-Mobile, Google, Anthropic, Tesla, Intel, or other companies is for informational purposes only and is not a recommendation to buy, sell, or hold any security.

Past performance is not indicative of future results. Investors should consider their own objectives, risk tolerance, time horizon, and liquidity needs before investing.

The views expressed are for informational and educational purposes only and are subject to change without notice.

This material is not intended as, and should not be interpreted as, individualized investment advice or a recommendation to buy, sell, or hold any security, sector, industry, or investment strategy.

References to specific companies, securities, sectors, or industries are for illustrative purposes only and should not be construed as investment recommendations.

Investing involves risk, including the possible loss of principal. Investments in a specific industry or sector may involve greater risk and volatility than more diversified investments.

Past performance is not indicative of future results. No investment strategy can guarantee a profit or protect against loss.

Forward-looking statements, including views about future demand, pricing, supply, or industry cycles, are based on current expectations and assumptions and are subject to risks and uncertainties. Actual results may differ materially.

Data and information are believed to be reliable, but accuracy, completeness, and timeliness are not guaranteed. Source documents should be retained for factual claims, third-party research references, and company-specific data.

Portfolio holdings, allocations, and risk budgets are subject to change based on market conditions, client objectives, and investment guidelines.

The author, firm, clients, or related persons may hold positions in securities mentioned and may buy or sell those securities without notice, subject to applicable policies and regulations.

Securities offered through LPL Financial, Member FINRA/SIPC. Investment Advice offered through WCG Wealth Advisors, LLC, an SEC Registered Investment Advisor. WCG Wealth Advisors, LLC and The Wealth Consulting Group are separate entities from LPL Financial. Index performance is shown for illustrative purposes only and does not predict or depict the performance of any investment. Past performance does not guarantee future results.

All information in this report is believed to be from reliable sources; however, WCG Wealth Advisors, LLC, makes no representation as to its completeness or accuracy.

In general, stock values fluctuate, sometimes widely, in response to activities specific to the companies as well as broad market, economic and political conditions. Stock investing involves risks, including fluctuating prices and loss of principal. Value investments can perform differently from the market as a whole. They can remain undervalued by the market for long periods of time. (135-LPL) International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets. (93-LPL)

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Bonds are subject to availability, change in price, call features and credit risk. (116-LPL)

The fast price swings in commodities will result in significant volatility in an investor’s holdings. Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors. (122-LPL)

Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss. (28-LPL)

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. (26-LPL)

Standard deviation is a historical measure of the variability of returns relative to the average annual return. If a portfolio has a high standard deviation, its returns have been volatile. A low standard deviation indicates returns have been less volatile. (131-LPL)

This is for educational / general purposes only, does not constitute investment, tax or legal advice and should not be relied on as such. This is not to be construed as an offer to buy or sell any financial instruments. Any strategies discussed are not intended to be relied upon as the sole factor in making an investment decision for any individual. As with all investments there are associated inherent risks. Please obtain and review all financial material carefully before investing. All material presented is compiled from sources believed to be reliable and current, but accuracy cannot be guaranteed. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested in directly. These comments should not be construed as recommendations but as an illustration of broader themes.

Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations. In addition, forward-looking statements, including index targets or market scenarios, are hypothetical in nature, reflect current views and assumptions and are subject to change based on market and economic conditions and are not guarantees of future performance. This is a hypothetical example and is not representative of any specific investment. Your results may vary. (88-LPL) Scenario outcomes are illustrative and not predictive. This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States. Indexes are unmanaged and cannot be invested in directly. (102-LPL)

Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

Publication Date: June 12, 2026

For Public Use in the US

The Wealth Consulting Group

LPL 1124206