MarketStrategy

by Talley Leger, Chief Market Strategist

May 22, 2026

Software vs. Semis: Skate to Where the Puck Is Going

Since April 2025, I’ve consistently opined about information technology, which remains a bright spot on the US economic landscape. Despite the tactical underperformance of the S&P 500 Information Technology sector from October 2025 to March 2026, I’ve maintained my long-held structural belief that tech companies have important roles to play. Specifically, technology itself should enable a broader stock market through increased efficiency, faster productivity and wider profit margins.

Despite bubble concerns, I still think that tech stocks are supported by tech fundamentals:

- According to the Census Bureau, manufacturers’ new orders for information technology accelerated 10.5% year-over-year (Y/Y) in March 2026, meaning the demand for computers and electronic products has grown at a double-digit pace.

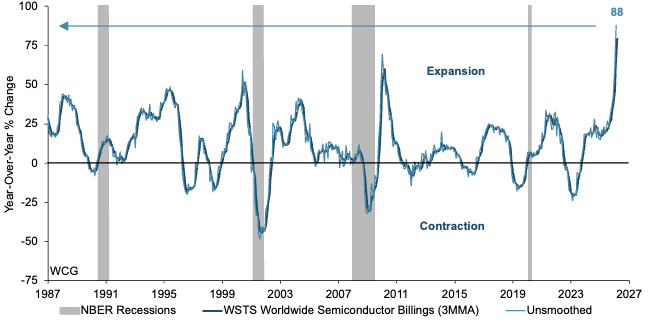

- According to World Semiconductor Trade Statistics (WSTS), worldwide semiconductor billings or revenues grew at a record-breaking pace of 88% Y/Y in March 2026 (see the chart below)!

- NVIDIA Corp. (NVDA) – the most valuable company on the planet with a market capitalization of over $5 trillion – delivered blowout performance in the first quarter with a $0.10 earnings per share (EPS) beat, a monstrous 136% Y/Y gain in EPS and revenues that soared 85% Y/Y to $81.62 billion. Moreover, management’s forward guidance of $91 billion beat Wall Street’s revenue estimates of $78.97 billion for the second quarter!

Global semi sales have grown 88% Y/Y, the fastest pace ever!

Sources:WSTS, WCG, 5/20/26.Notes: NBER = National Bureau of Economic Research. WSTS = World Semiconductor Trade Statistics. MMA = Month moving average.

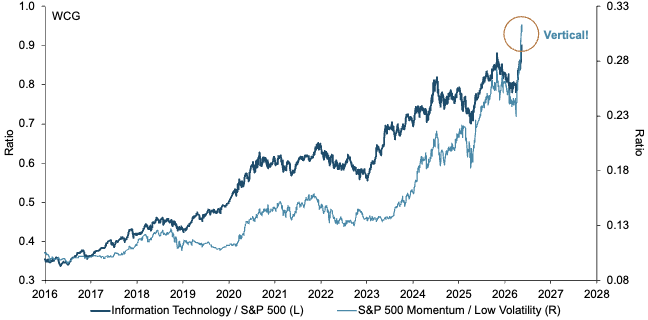

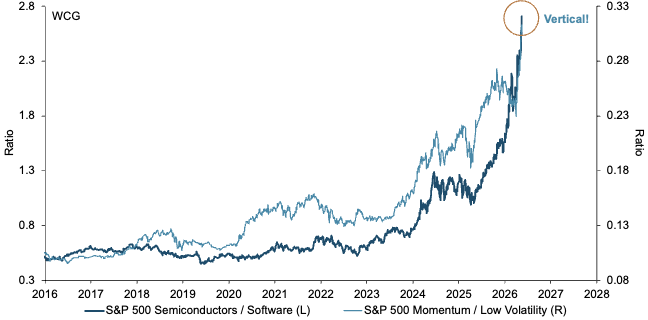

Everybody loves semiconductor companies, including us. Indeed, the surge in tech, semi and momentum stocks since March 2026 has ratified our optimistic outlook. As such, the forward-looking growth investor in me is emboldened by those stellar results (see the charts below).

That said, the prudent risk manager in me recommends trimming positions and protecting gains at this stage. Meanwhile, the contrarian value investor in me discourages overlooking the lagging areas of the stock market that could benefit from another “catchup” phase, including software and low volatility stocks.

Psychologists and neuroscientists consider such “self-directed speech” a sign of a functional, active brain :) In my view, those “inner voices” are simply manifestations of a multi-dimensional, cross-disciplinarian process that considers many different investment styles and objectives at the same time.

Sectors: An Old Economy Revival

As discussed last week, I still believe the tech sector should pull the rest of the stock market along for the ride across the style, size and sector spectrums. Indeed, my “tech enablement” thesis is evolving in real-time: Massive capital expenditure (capex) on artificial intelligence (AI) and cloud infrastructure has created “ripple” effects across other areas of the stock market and economy. For example, the S&P 500 Industrials, Materials and Utilities sectors are direct beneficiaries of the data center buildout, energy grid modernization and supply chain optimization. Tech-adjacent companies in those old-economy sectors are managing overhead, improving operational leverage and expanding margins.

Tech should pull the rest of the stock market along for the ride

Sources: S&P Global, YCharts, WCG, 5/18/26. Notes:Indices are unmanaged and cannot be invested in directly. Past performance does not guarantee future results.

Industries & Factors: Mo F’Sho

All industries and factors are not created equal.

- Leaders: The S&P 500 Semiconductors & Semiconductor Equipment industry and the S&P 500 Momentum Index (which focuses on stocks with the fastest price momentum) have had truly historic runs (see the surrounding charts).

- Laggards: By contrast, the S&P 500 Software & Services industry (which has been quietly “basing” since 1Q26) and the S&P 500 Low Volatility Index (which focuses on stock prices with the lowest standard deviations over the last 12 months) have been left in the wake of the semi frenzy.

It’s no coincidence that the outperformance of semiconductors versus software tracks the outperformance of momentum versus low volatility. The information technology sector represents almost 50% of the S&P 500 Momentum Index. Furthermore, Nvidia Corp. (NVDA), Broadcom, Inc. (AVGO), Micron Technology, Inc. (MU) and Advanced Micro Devices (AMD) are among that index’s top 10 constituents by weight. In my humble opinion, it’s reasonable to expect a period of consolidation in semi and momentum stocks to digest their “exponential” gains before the next move higher.

On the flip side, a window of opportunity could open for mature, stable and profitable software & services companies that’ve been overlooked by investors. True, traditional defensive sectors such as utilities (27%), consumer staples (11%) and health care (7%) dominate the low volatility factor. However, we’re intrigued by Oracle Corp. (ORCL), which has a highly recurring revenue model and deep enterprise entrenchment, as well as Akamai Technologies, Inc. (AKAM), which is a steady, essential service provider with reliable cashflow and a defensive market position.

The momentum trade is crowded in semiconductors

Sources:S&P Global, YCharts, WCG, 5/18/26. Notes:Shaded areas are US recessions. Indices are unmanaged and cannot be invested in directly. Past performance does not guarantee future results.

Software Applications: The Jevons Paradox

In the 19th century, economist William Stanley Jevons observed that technological improvements increasing the efficiency of coal usage didn’t decrease coal consumption. Rather, those enhancements made coal cheaper and more useful, thereby fueling a significant increase in coal demand. The Jevons Paradox applies directly to software today.

AI: Disruptor or Accelerant?

Many investors fear generative AI as an existential threat to legacy software, assuming Large Language Models (LLMs) and other tools will automate routine tasks and destroy industry pricing power. That view misunderstands the economics of technological efficiency, which should make it dramatically cheaper, faster and easier to write code and create new applications. By lowering the cost of production, AI could stoke demand for software solutions across every corner of the economy. AI allows software companies to cut costs and expand profit margins while simultaneously satisfying a wider array of consumer and enterprise needs.

Software Employment: Creative Destruction

In the mid-20th century, economist Joseph Schumpeter described “creative destruction” as the essential capitalist process whereby radical innovation dismantles established systems to make way for new, more dynamic economic growth. In the context of the software labor market, generative AI is the ultimate engine of that destruction: It automates basic, rote coding tasks and simultaneously creates higher-value demand for complex system integration, data security and AI oversight.

According to the Bureau of Labor Statistics (BLS), computing infrastructure providers, data processing, web hosting and related services employment fell by -4,000 or -1% month-over-month (M/M) in April 2026. The same employment category has seen a cumulative decrease of -31,500 jobs or -6% from its peak in August 2023.

However, the BLS projects a cumulative increase of 287,900 jobs or 15% growth (which is much faster than the national average) in the demand for software developers and quality assurance analysts through 2034. Excluding replacement needs, those figures translate to 28,790 net new job openings annually that didn’t exist before the AI and cloud buildout.*

Bottom Line

If AI were to completely displace developers, I doubt the demand outlook for software professionals would be so robust. While AI automates rote coding tasks, it may “parabolically” increase the need for system integration, data pipeline management, security and AI oversight. Ultimately, AI isn’t eliminating software jobs … it’s simply destroying the old coding paradigm to birth a larger, more sophisticated workforce. While the human capital required to build and maintain our future software ecosystem is shifting, the aggregate demand for augmented humans may surpass even my wildest hopes and dreams.

*BLS, Occupational Outlook Handbook: Software Developers, Quality Assurance Analysts, and Testers, August 28, 2025.

Recent and relevant Market Strategy Flashes:

“Tech Enablement:” Why Strong Sales Drive Strong CapEx, May 15, 2026

Our “Four-Banger” Growth Engine Is Humming, May 8, 2026

Doing More With Less: Why S&P 500 Employees Are 3x More Productive Than the Average US Worker, February 6, 2026

Profit Paradox: Why Slow Hiring Boosts the S&P 500, January 16, 2026

Technology itself should enable a broader market, October 24, 2025

AI: The force that could extend and end the cycle, October 8, 2025

Productivity: The silver lining of meagre job growth, October 3, 2025

AI revolution: Boosting productivity, expanding margins, August 8, 2025

From beta grazing to alpha hunting, June 13, 2025

The silver lining of slowing payroll growth, November 5, 2024

PortfolioStrategy

by Jim Worden, CFA®, CMT®, CAIA®, Chief Investment Officer

May 22, 2026

Thoughts on the Markets

The big news recently was NVIDIA’s earnings report. Compared with last year, revenue was up 85%. When we break out Data Center revenue, revenue was up 92%. GAAP net income was $58.3 billion, up 211% from the year before. We will look for NVIDIA’s market reaction today and the reaction of other AI-adjacent companies. As of this writing, NVIDIA is up 0.38%. Despite the amazing quarter, investor expectations were already elevated. NVIDIA reported fiscal first-quarter revenue of $81.6 billion, Data Center revenue of $75.2 billion, and GAAP net income of $58.3 billion.

I recently got back from several productive meetings in New York City, where I met with some of the largest asset managers in the world. Of the nine companies I met with, every single one had something to say about AI.

We practically cannot turn around without hearing something from someone about AI. People’s views on it vary. There is fear and worry, but also a great deal of excitement around it. If we listen to some of the smartest minds on the AI topic, it can also be hard to digest.

Those who know me well know that I am an eternal optimist. That doesn’t mean that I’m a perma-bull when it comes to markets when things look rich. It means that I’m generally very optimistic that things in the future will be better than they have been in the past. But I also try to stay as grounded as possible and acknowledge the reality that we live in.

So, when I hear smart people say things like:

- “Work will be optional”

- “The economy will double in size in five years”

- “Those who are displaced will get universal basic income”

I have a tendency to question the details. We can be optimistic while also questioning things that seem unreasonable.

So, I asked AI to critique these assumptions about AI. I gave 11 different large language models (LLMs) the same prompt, asking about optional work, the economy doubling, and the prospect of universal basic income for those who are displaced. After aggregating the 11 responses, I asked three models that score well — Anthropic’s Claude Opus, OpenAI’s ChatGPT 5.5, and Google’s Gemini 3.5 — to summarize the results, compare the responses, and identify what was missed, exaggerated, or wrong. The analysis included economic formulas and discussions on labor, productivity, and GDP growth. It also included data from Acemoglu, MIT, 2024; Goldman Sachs, 2023; Penn Wharton, 2025; IMF, 2024; McKinsey, 2023; and IFR World Robotics, 2024. I further asked the models to separate fact from opinion.

On optional work and Universal Basic Income

The premise is that robots will do much of the work that humans don’t want to do. There is also a premise that some jobs will be replaced, even for people who want to work.

One model cited that society would want capital investment in robots ex ante, but robots would need to be heavily taxed once they exist in order to fund UBI ex post. Rational investors would underinvest, anticipating the high tax. This would create a time-inconsistency problem. The model suggested that the robots would have to be publicly owned before any collapse in wages. UBI would then become a dividend, not a tax. But this would require a major shift in how institutions think about and approach the problem.

Another model cited Henry Ford and the “realization crisis,” meaning that workers with low or no wages would not be able to buy what robots produce, making the robots less valuable. A conclusion from this analysis suggests that this is more a function of politics than economics.

Finally, another model invoked comparative advantage and how it could disappear due to the energy required to supply and maintain robots in one region while they operate in another region.

On the economy doubling in size in five years

For the economy to double in five years, real GDP would need to grow by roughly 14.9% annually. The U.S. has averaged roughly 3% annual GDP growth since 1947, according to MIT News. Goldman Sachs estimated that generative AI could raise global GDP by 7%, or almost $7 trillion, and lift productivity growth by 1.5 percentage points over a 10-year period. Daron Acemoglu of MIT estimated a much more modest GDP impact from AI over 10 years. MIT News summarizes his published Economic Policy paper as estimating a 1.1% to 1.6% GDP increase over the next decade, with roughly a 0.05% annual gain in productivity.

The math just doesn’t add up. There is also the question of labor and capital in the GDP formula. If labor declines, will capital make up the difference? And will that come remotely close to doubling the economy in five years?

AI scenario written by AI, in my style, per Claude

“I went into this exercise skeptical of the AI-utopia narrative, and I came out roughly where I started, but with a few sharper distinctions.

First, the headline claim — the economy doubling in five years, work becoming optional, and UBI for all — is not internally incoherent. It is conditional. It requires a chain of assumptions that includes broad AGI capability, near-frictionless physical deployment, an unprecedented institutional shift in capital ownership, and global cooperation on technology diffusion and taxation. Each link in that chain is independently uncertain, and the joint probability is meaningfully lower than the consumer press suggests.

Second, the more realistic forward path — supported by Acemoglu, Penn Wharton, Goldman, and the IMF — is modest measured productivity gains over a decade, concentrated in a relatively narrow set of cognitive-task categories, with substantial near-term inequality pressure and a long tail of physical deployment that takes 20-plus years rather than five. Penn Wharton estimates that AI will increase productivity and GDP by 1.5% by 2035, nearly 3% by 2055, and 3.7% by 2075. The IMF has also noted that AI is likely to affect advanced economies sooner than emerging-market and developing economies because of their greater exposure to cognitive-intensive roles.

Third, the global story matters more than the domestic one for portfolio construction. If labor-arbitrage manufacturing is increasingly automated, the investment thesis for many emerging-market economies needs to be re-underwritten. Resource exposure — copper, lithium, rare earths, uranium, and natural gas — becomes structurally more important. So does identifying which countries actually own the AI and robotics capital stack versus which countries are downstream.

Fourth, the financial planning conversation with our clients should not assume any version of this future. The base case remains a world where work matters, savings matter, and tax policy on capital is a live political question for the next decade. The optionality on a more transformative outcome is real, but it is optionality — not a forecast.

I remain an optimist about AI. Several studies suggest measurable productivity gains are emerging, particularly in areas such as coding, analysis, customer service, research, and design. But the leap from ‘a useful general-purpose technology’ to a ‘work-optional, post-scarcity utopia in five years’ skips over a lot of ownership, transition, demand, energy, and political-economy work that no one has actually done yet.

Connecting the dots requires the dots to be there. On the most aggressive version of the AI-utopia narrative, several of the dots have not yet been drawn.”

My summary

Having gone through this exercise, and knowing full well that these tools are not yet perfect, I take some comfort that some of the sound bites we may hear about both AI fears and AI utopia are not completely grounded in data that is clear and highly probable. I believe AI will continue to evolve and may help solve many of our country’s and the world’s challenges, whether that means finding cures for diseases, helping people live longer, lifting others out of poverty, or creating more opportunities to help and serve others. Markets will likely continue to find ways to figure it all out and connect the dots as they become apparent. It will likely mean we get some things wrong, but we may also get an awful lot of things right.

Source Notes

Acemoglu: Daron Acemoglu’s AI-growth estimate is summarized by MIT News as a 1.1% to 1.6% increase in GDP over 10 years, with roughly a 0.05% annual gain in productivity. The earlier MIT-hosted version of The Simple Macroeconomics of AI includes lower upper-bound estimates after adjusting for harder-to-learn tasks.

Goldman Sachs: Goldman Sachs Research estimated in 2023 that generative AI could raise global GDP by 7%, or almost $7 trillion, and lift productivity growth by 1.5 percentage points over a 10-year period.

Penn Wharton: Penn Wharton Budget Model estimated in 2025 that AI could increase productivity and GDP by 1.5% by 2035, nearly 3% by 2055, and 3.7% by 2075.

IMF: The IMF’s 2024 Staff Discussion Note, Gen-AI: Artificial Intelligence and the Future of Work, focuses on labor-market exposure, inequality, and the likelihood that advanced economies will experience AI’s effects sooner because of their employment mix.

McKinsey: McKinsey’s 2023 report, The Economic Potential of Generative AI: The Next Productivity Frontier, estimated that generative AI could add $2.6 trillion to $4.4 trillion annually across 63 use cases, while also noting that realizing productivity benefits will require worker transitions and investment.

IFR World Robotics: The International Federation of Robotics’ World Robotics 2024 report recorded 4,281,585 industrial robots operating in factories worldwide, up 10%, with annual installations exceeding 500,000 units for the third consecutive year.

Definitions

Artificial intelligence (AI): Technology designed to perform tasks that typically require human intelligence, such as language processing, pattern recognition, prediction, coding, and decision support.

Large language model (LLM): A type of AI model trained on large amounts of text and other data to generate, summarize, classify, translate, and analyze information.

Artificial general intelligence (AGI): A theoretical form of AI that could perform a broad range of intellectual tasks at or above human capability. There is no universally accepted definition or timeline for AGI.

Universal Basic Income (UBI): A policy concept in which individuals receive a recurring cash payment, typically from the government, regardless of employment status or income level.

Gross Domestic Product (GDP): The total value of goods and services produced within an economy over a specific period.

Real GDP: GDP adjusted for inflation.

Productivity: A measure of output produced per unit of input, often measured as output per worker or output per hour worked.

GAAP: Generally Accepted Accounting Principles, the accounting standards used by U.S. public companies for financial reporting.

Data Center revenue: Revenue generated from products and services used in data centers, including computing, networking, and AI infrastructure.

Ex ante / ex post: “Ex ante” means before the fact, while “ex post” means after the fact.

Comparative advantage: An economic concept in which a person, company, or country can produce a good or service at a lower opportunity cost than another.

Labor arbitrage: The practice of locating production or services where labor costs are lower.

Post-scarcity: A theoretical economic condition in which most goods and services become so abundant that scarcity is greatly reduced or eliminated.

Disclosures

This material is for informational and educational purposes only and should not be construed as investment, tax, legal, or accounting advice. It does not constitute a recommendation to buy or sell any security, investment product, sector, asset class, or strategy.

The views expressed are opinions as of the date written and are subject to change without notice. Forward-looking statements, including comments about artificial intelligence, economic growth, productivity, labor displacement, market outcomes, and future investment implications, are inherently uncertain and may not occur as expected.

References to NVIDIA or any other company are for illustrative purposes only and should not be interpreted as a recommendation or endorsement. Individual securities mentioned may or may not be held in client portfolios.

AI-generated outputs may contain errors, omissions, unsupported assumptions, or outdated information. The model comparisons discussed above reflect this specific exercise and should not be interpreted as a comprehensive ranking of AI models or a guarantee of model quality or reliability.

Past performance is not indicative of future results. Economic forecasts, productivity estimates, and market expectations are inherently uncertain and may differ materially from actual outcomes.

Securities offered through LPL Financial, Member FINRA/SIPC. Investment Advice offered through WCG Wealth Advisors, LLC, an SEC Registered Investment Advisor. WCG Wealth Advisors, LLC and The Wealth Consulting Group are separate entities from LPL Financial. Index performance is shown for illustrative purposes only and does not predict or depict the performance of any investment. Past performance does not guarantee future results.

All information in this report is believed to be from reliable sources; however, WCG Wealth Advisors, LLC, makes no representation as to its completeness or accuracy.

In general, stock values fluctuate, sometimes widely, in response to activities specific to the companies as well as broad market, economic and political conditions. Stock investing involves risks, including fluctuating prices and loss of principal. Value investments can perform differently from the market as a whole. They can remain undervalued by the market for long periods of time. (135-LPL) International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets. (93-LPL)

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Bonds are subject to availability, change in price, call features and credit risk. (116-LPL)

The fast price swings in commodities will result in significant volatility in an investor’s holdings. Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors. (122-LPL)

Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss. (28-LPL)

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. (26-LPL)

Standard deviation is a historical measure of the variability of returns relative to the average annual return. If a portfolio has a high standard deviation, its returns have been volatile. A low standard deviation indicates returns have been less volatile. (131-LPL)

This is for educational / general purposes only, does not constitute investment, tax or legal advice and should not be relied on as such. This is not to be construed as an offer to buy or sell any financial instruments. Any strategies discussed are not intended to be relied upon as the sole factor in making an investment decision for any individual. As with all investments there are associated inherent risks. Please obtain and review all financial material carefully before investing. All material presented is compiled from sources believed to be reliable and current, but accuracy cannot be guaranteed. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested in directly. These comments should not be construed as recommendations but as an illustration of broader themes.

Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations. In addition, forward-looking statements, including index targets or market scenarios, are hypothetical in nature, reflect current views and assumptions and are subject to change based on market and economic conditions and are not guarantees of future performance. This is a hypothetical example and is not representative of any specific investment. Your results may vary. (88-LPL) Scenario outcomes are illustrative and not predictive. This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States. Indexes are unmanaged and cannot be invested in directly. (102-LPL)

Publication Date: May 22, 2026

For Public Use in the US

The Wealth Consulting Group

LPL 1113593